Introduction

International money transfer fees can quietly reduce your income if you work with global clients, send money to family, pay contractors, or run an online business. A transfer may look simple on the surface: the sender enters an amount, chooses a recipient, and sends the payment. But behind that transaction, there can be several different costs.

You may pay a visible transfer fee. You may lose money through an exchange-rate markup. Your bank may charge an incoming wire fee. An intermediary bank may deduct money before the payment reaches you. A payment platform may charge withdrawal fees. If the transfer is funded by card, the cost may be higher than a bank-funded transfer.

That is why comparing international money transfer fees is important. The cheapest option is not always the one that says “zero fee.” Sometimes a provider charges no upfront fee but gives a weaker exchange rate. Another provider may show a small fee but use a better exchange rate, which means the recipient receives more money.

This guide compares banks, Wise, Payoneer, Remitly, and online payment apps from the point of view of freelancers, remote workers, small businesses, and people receiving international payments.

The goal is not to promote one provider for every situation. The goal is to help you understand how international transfer costs work, what fees to check, and how to choose the best payment method for your country, currency, and client type.

What Are International Money Transfer Fees?

International money transfer fees are the costs charged when money moves from one country or currency to another. These fees can apply when you send money abroad, receive money from a foreign client, withdraw funds from a payment platform, or convert one currency into another.

The main types of international transfer costs include:

- Transfer fees

- Currency conversion fees

- Exchange-rate markups

- Incoming wire fees

- Outgoing wire fees

- Intermediary bank fees

- Payment method fees

- Withdrawal fees

- Card processing fees

- Platform fees

For freelancers and online businesses, even a small percentage can become expensive. If you receive $2,000 per month from international clients and lose 3% in transfer and conversion costs, that is $60 per month or $720 per year. If you lose 6%, that becomes $1,440 per year.

That money could have paid for:

- Software subscriptions

- Website hosting

- Advertising

- Taxes

- Business savings

- Emergency funds

- Contractor payments

Why Transfer Fees Are Confusing

International money transfer fees are confusing because the total cost is not always shown in one place.

A provider may advertise a low transfer fee, but the exchange rate may include a markup. A bank may say it charges a flat wire fee, but another bank in the middle may also deduct money. A payment app may show the recipient amount before final bank deductions.

This is why you should never compare providers by visible transfer fee only. You should compare the final amount the recipient receives after all costs.

For example, imagine you send $1,000 from the United States to another country.

- Provider A charges no transfer fee but gives a weaker exchange rate.

- Provider B charges a $7 fee but gives a stronger exchange rate.

Provider B may still be cheaper if the recipient receives more money at the end.

The real question is not:

Which provider has the lowest fee?

The better question is:

How much money will arrive after fees, exchange rates, and withdrawal costs?

The Main Costs Behind International Transfers

1. Transfer Fee

The transfer fee is the visible charge for sending money. It may be a fixed amount, a percentage of the transfer, or a combination of both.

Common examples include:

- $5 per transfer

- 1% of the transfer amount

- $3 plus 0.5%

- No upfront fee but weaker exchange rate

Transfer fees often depend on:

- Destination country

- Sending country

- Payment method

- Delivery speed

- Currency

- Transfer amount

2. Exchange-Rate Markup

The exchange-rate markup is one of the most important hidden costs. This happens when a provider converts money using a rate that is worse than the real market rate.

For example, if the real exchange rate is:

1 USD = 280 PKR

A provider may convert at:

1 USD = 273 PKR

The difference may not look like a fee, but it is still a cost.

This is why freelancers should always compare:

- The visible transfer fee

- The exchange rate

- The final received amount

- The withdrawal cost

Do not look only at the upfront fee. The exchange rate can make a big difference.

3. Wire Transfer Fees

Traditional banks often use international wire networks. These can be secure and widely accepted, but they may also be expensive.

Wire transfer costs may include:

- Outgoing wire fee

- Incoming wire fee

- Intermediary bank fee

- Currency conversion fee

- Exchange-rate markup

Wire transfers are often used for:

- Large business payments

- Real estate transactions

- Corporate payments

- Legal payments

- Formal bank-to-bank transfers

For freelancers and small businesses, however, wire fees can be painful when payment amounts are small.

4. Intermediary Bank Fees

When money moves through the international banking system, it may pass through one or more intermediary banks. These banks can deduct fees before the funds reach the recipient.

This is frustrating because the sender and recipient may not know the exact deduction in advance.

For example:

- Client sends: $1,000

- Intermediary bank deducts: $15

- Receiving bank deducts: $10

- Freelancer receives: $975

This is why freelancers should be careful when accepting international wire transfers for small invoices.

5. Payment Method Fees

How the sender funds the transfer can affect the cost.

Some payment methods are cheaper. Others are faster but more expensive.

Providers may charge different fees for:

- Bank account transfers

- Debit card payments

- Credit card payments

- Cash pickup

- Mobile wallet payments

- Payment gateway transfers

If your client is paying you as a freelancer, bank transfer or local receiving account details are often cheaper than card-funded payments.

6. Withdrawal Fees

For freelancers, receiving money is only part of the journey.

You may receive money into:

- Wise

- Payoneer

- PayPal

- Skrill

- A freelance marketplace wallet

- A payment gateway

- A multi-currency business account

Then you may need to withdraw it to your local bank.

Withdrawal fees can be:

- Fixed fees

- Percentage-based fees

- Currency conversion fees

- Exchange-rate markups

- Local bank receiving fees

Some platforms also charge different fees depending on whether you withdraw in the same currency or convert to another currency.

Banks vs Online Money Transfer Providers

Traditional banks and online money transfer providers serve different needs.

Banks are often trusted, regulated, and useful for formal business banking. Online transfer providers are often faster, cheaper, and more transparent for cross-border payments.

Traditional Banks

Banks are still useful for large transfers, formal business payments, and situations where the sender or recipient needs a traditional bank record.

Many businesses prefer bank transfers because they feel official and easy to document.

However, international bank transfers can be expensive. Banks may charge outgoing wire fees, incoming fees, intermediary fees, and exchange-rate markups. They may also take several business days to deliver funds.

Pros of Banks

- Trusted and widely accepted

- Useful for large business transfers

- Good for official documentation

- Suitable for registered companies

- Can support compliance-heavy payments

- Strong local banking relationship

Cons of Banks

- Higher wire fees

- Exchange-rate markups

- Possible intermediary bank deductions

- Slower delivery times

- Less transparent total cost

- Not ideal for small freelance payments

Online Money Transfer Providers

Online money transfer providers are built specifically for sending and receiving money across borders. They often show the fee, exchange rate, and expected received amount before the transfer is confirmed.

Popular options include:

- Wise

- Remitly

- Payoneer

- Western Union digital transfers

- WorldRemit

- Revolut

- PayPal

- Regional money transfer apps

The best provider depends on the sending country, receiving country, currency, payment method, and delivery option.

Pros of Online Transfer Providers

- Often cheaper than banks

- More transparent pricing

- Faster delivery in many corridors

- Useful mobile apps

- Multiple delivery options

- Good for freelancers and remote workers

- Better for small and medium transfers

Cons of Online Transfer Providers

- Availability varies by country

- Limits may apply

- Verification may be required

- Fees vary by payment method

- Not always ideal for large corporate transfers

- Some providers may not support business payments in all regions

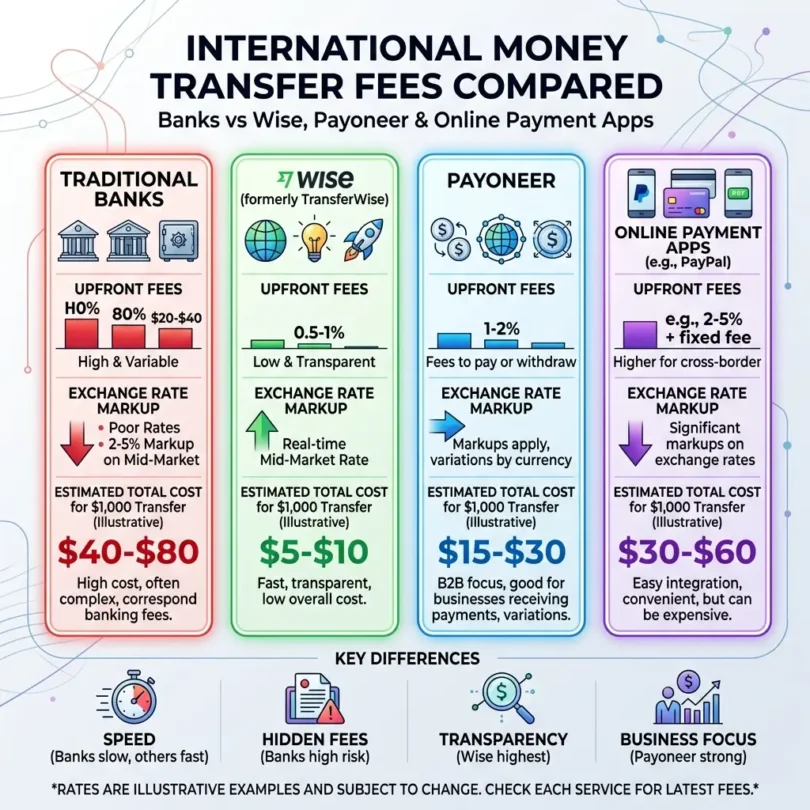

Wise International Transfer Fees

Wise is popular because it focuses heavily on transparent exchange rates and international transfers. Many freelancers use Wise because it can help them receive and convert foreign currencies with clearer pricing than traditional banks.

Wise may be useful if you:

- Receive payments from international clients

- Want to hold multiple currencies

- Prefer transparent exchange-rate information

- Need local account details in supported countries

- Want to convert money before withdrawing

- Send money to contractors or suppliers

Wise usually shows:

- The conversion rate

- The transfer fee

- The expected received amount

- The payment method cost

- The estimated delivery time

This is helpful because you can see the real cost before sending or receiving money.

However, Wise is not available in every country for every feature. Some users can receive account details, while others may have limited access depending on location and regulations.

Best Use Case for Wise

Wise is best for freelancers and small businesses that invoice clients directly and want clear foreign exchange costs.

Example:

A freelancer invoices a UK client in GBP, receives the money into a GBP balance, converts part of it to local currency, and keeps the rest for future expenses.

Payoneer International Payment Fees

Payoneer is widely used by freelancers, marketplace sellers, affiliate marketers, agencies, and online businesses. It is common among users who receive payments from platforms like freelance marketplaces, ecommerce platforms, ad networks, and international companies.

Payoneer may be useful if you:

- Work with global marketplaces

- Receive USD, EUR, GBP, or other supported currencies

- Need local receiving account details

- Want to withdraw to a local bank

- Pay contractors or suppliers

- Receive payments from companies that already support Payoneer

Payoneer fees can vary depending on:

- How you receive money

- Which currency you receive

- How you withdraw funds

- Whether currency conversion is involved

- Whether the client pays by card or bank transfer

- Your country and account type

Some Payoneer-to-Payoneer payments may be low-cost or free, while card-funded payments or certain withdrawals may cost more.

Best Use Case for Payoneer

Payoneer is best for freelancers who receive marketplace payments or international business payments from companies already using Payoneer.

Example:

A freelance designer receives USD from a US client through local receiving details, keeps the balance in Payoneer, and withdraws to a local bank when needed.

Remitly and Remittance Apps

Remitly and similar remittance apps are often used for personal transfers, especially when people send money to family abroad.

These apps may offer:

- Bank deposits

- Mobile wallet transfers

- Cash pickup

- Home delivery in some countries

- Fast delivery options

- Economy delivery options

Remitly-style apps can be useful when:

- The recipient needs money quickly

- Cash pickup is important

- Mobile wallet delivery is available

- The sender wants an easy app experience

- The transfer is personal rather than business-related

However, freelancers should be careful. Some remittance apps are designed for personal transfers, not business invoices.

If you are receiving client payments, check whether:

- The provider allows business-related payments

- The transaction record is suitable for accounting

- The transfer can be documented for taxes

- Your account will not be restricted for business use

Best Use Case for Remittance Apps

Remittance apps are best for personal transfers and family support payments, not always for professional freelance income.

Example:

A worker abroad sends monthly family support to a relative’s local bank or mobile wallet.

PayPal and Online Payment Apps

PayPal is one of the most recognized online payment platforms in the world. Many clients are comfortable using it, especially for small digital services, online purchases, and freelance payments.

However, PayPal fees and currency conversion costs can be higher than other options in some countries.

PayPal may be useful if:

- Your client strongly prefers PayPal

- You sell digital services online

- You need quick payment links

- You accept card-style payments

- You work with clients who do not want to use bank transfer

- You need a simple invoice payment option

But freelancers should compare the cost carefully. PayPal may include:

- Receiving fees

- Currency conversion charges

- Withdrawal fees

- Exchange-rate differences

- Business account fees in some cases

Other online payment apps may include:

- Skrill

- Stripe

- Revolut

- Cash App

- Venmo

- Zelle

- Regional wallets

Availability depends on country, and not every app supports international business payments.

Best Use Case for PayPal and Payment Apps

PayPal and payment apps are useful when client convenience matters more than the lowest possible fee.

Example:

A client wants to pay a freelancer quickly using a PayPal invoice or payment link.

International Wire Transfer Fees

International wire transfers are common for bank-to-bank payments. They are often used by companies, legal firms, institutions, real estate buyers, and businesses sending larger amounts.

Wire transfers may include:

- Sender bank fee

- Recipient bank fee

- Intermediary bank fee

- Exchange-rate markup

- SWIFT-related charges

- Currency conversion charges

For large transfers, a wire may be acceptable because the fee becomes a smaller percentage of the total amount.

For small freelancer payments, wire fees can be too expensive.

Example:

- $30 wire fee on a $5,000 payment = 0.6%

- $30 wire fee on a $300 payment = 10%

That is why wire transfers are usually not ideal for small recurring freelance invoices.

Bank Transfer vs Wise vs Payoneer vs PayPal

Here is a simple practical comparison.

Bank Transfers

Best for:

- Large payments

- Formal business transfers

- Local bank-to-bank payments

- Registered businesses

- Clients who only pay by bank

- Compliance-heavy payments

Main concern:

Wire fees, exchange-rate markups, and intermediary bank deductions.

Wise

Best for:

- Transparent currency conversion

- International freelancers

- Multi-currency balances

- Direct client invoices

- Lower-cost cross-border transfers

- Holding USD, EUR, or GBP

Main concern:

Feature availability varies by country.

Payoneer

Best for:

- Freelance marketplaces

- Platform payments

- International business receiving accounts

- USD, EUR, GBP receiving details

- Global freelancer payments

- Contractor payments

Main concern:

Fees vary by payment method and withdrawal type.

PayPal

Best for:

- Client convenience

- Payment links

- Small online services

- Digital products

- Fast payments

- Clients who prefer card-style payments

Main concern:

Fees and currency conversion may be higher.

Remittance Apps

Best for:

- Personal transfers

- Family support payments

- Cash pickup

- Mobile wallet delivery

- Fast remittances

Main concern:

Not always suitable for professional freelance invoices.

How Freelancers Should Choose an International Payment Method

Freelancers should choose payment methods based on cost, convenience, country support, and professional recordkeeping.

Here is a simple decision framework.

If Your Client Is in the US

Consider USD receiving details through a multi-currency account or payment platform. This can make it easier for the client to pay you like a local business.

Useful options may include:

- Wise

- Payoneer

- Local bank wire

- PayPal

- ACH-supported platforms

If Your Client Is in Europe

EUR payments through SEPA or EUR account details may reduce costs. If you can provide EUR receiving details, the client may avoid international wire complexity.

Useful options may include:

- Wise

- Payoneer

- Revolut Business

- Traditional bank transfer

- SEPA-supported platforms

If Your Client Is in the UK

GBP local receiving details can help reduce transfer friction.

Useful options may include:

- Wise

- Payoneer

- Revolut Business

- Bank transfer

- PayPal

If Your Client Wants to Pay by Card

A payment gateway, PayPal invoice, Stripe invoice, or payment link may be convenient. However, card payments usually cost more than bank transfers.

Before accepting card payments, decide whether:

- You will absorb the fee

- You will include the cost in your pricing

- You will offer bank transfer as a lower-cost option

- You will use card payments only for selected clients

If You Work Through Freelance Marketplaces

Use the platform’s supported withdrawal methods and compare costs.

Some platforms support:

- Payoneer

- Bank withdrawal

- PayPal

- Local transfer methods

- Marketplace wallet balance

Check:

- Withdrawal fee

- Currency conversion rate

- Minimum withdrawal amount

- Processing time

- Local bank charges

- Payment hold period

How to Reduce International Money Transfer Fees

Freelancers and small businesses can reduce fees by choosing payment methods carefully.

1. Use Local Receiving Details When Possible

If your provider gives you local account details for USD, EUR, or GBP, use them when they match your client’s country. This can reduce the need for international wires.

Local receiving details may help you receive:

- USD from US clients

- GBP from UK clients

- EUR from European clients

- AUD from Australian clients

- CAD from Canadian clients

2. Compare the Final Received Amount

Do not compare only the fee. Compare how much money arrives after transfer fees, exchange rates, and withdrawal charges.

Before choosing a provider, check:

- Sending fee

- Receiving fee

- Exchange rate

- Conversion fee

- Withdrawal fee

- Delivery time

- Final received amount

3. Avoid Unnecessary Currency Conversions

If you receive USD and also pay for software in USD, keep some money in USD instead of converting everything immediately.

This can help reduce repeated conversion costs.

For example, you may use USD balance for:

- Hosting

- SaaS tools

- Domain renewals

- Paid ads

- Contractor payments

- Software subscriptions

4. Use Bank Transfers Instead of Cards When Cheaper

Card-funded transfers are often more expensive than bank-funded transfers. If speed is not urgent, bank funding may reduce costs.

Ask your client if they can pay by:

- ACH

- SEPA

- Local bank transfer

- Business bank transfer

- Multi-currency account details

5. Withdraw Larger Amounts Less Often

If your platform charges fixed withdrawal fees, withdrawing larger amounts less frequently may reduce total costs.

For example:

- Four withdrawals of $250 may cost more.

- One withdrawal of $1,000 may cost less.

However, do not keep too much money in a platform if you need better security or local access.

6. Keep a Local Business Bank Account

A local business bank account helps you:

- Receive withdrawals

- Pay local expenses

- Manage taxes

- Keep records clean

- Separate personal and business money

- Build a professional banking history

7. Read Fee Pages Regularly

Fees change. Before choosing a provider, check the latest pricing page and country-specific terms.

You should review:

- Transfer fees

- Currency conversion fees

- Receiving fees

- Withdrawal fees

- Inactivity fees

- Card fees

- Business account charges

Best International Transfer Method for Freelancers

The best method depends on your situation, but many freelancers can use this structure:

- Use Wise or Payoneer for international receiving.

- Use a local bank account for local withdrawals.

- Use PayPal only when clients prefer it.

- Use payment gateways for card payments.

- Use bank wires for large formal transfers.

- Use remittance apps mainly for personal transfers.

This setup gives flexibility and helps reduce payment risk.

Example Freelancer Payment Setup

Imagine a freelance SEO consultant working with clients in the US, UK, and Europe.

A smart setup may look like this:

- US clients pay to USD receiving details.

- UK clients pay to GBP receiving details.

- EU clients pay to EUR receiving details.

- The freelancer holds balances in the original currency.

- The freelancer converts money when rates are reasonable.

- Local withdrawals go to a business bank account.

- Tax savings are moved into a separate account.

- Software subscriptions are paid from the same currency balance.

This system reduces unnecessary conversions, keeps records clean, and helps the freelancer understand true profit.

Common Mistakes to Avoid

Mistake 1: Choosing the Provider With “Zero Fees”

Zero fee does not always mean cheapest. The exchange rate may include a hidden markup.

Always compare the final received amount.

Mistake 2: Ignoring Incoming Bank Fees

Your client may pay the transfer fee, but your bank may still deduct an incoming fee.

Before accepting bank transfers, check:

- Incoming international wire fee

- Currency conversion fee

- Intermediary bank deduction

- Local bank receiving charges

Mistake 3: Using Wire Transfers for Small Payments

Wire transfers can be too expensive for small freelance invoices.

For smaller payments, consider:

- Local receiving details

- Multi-currency accounts

- Marketplace withdrawal options

- Lower-cost transfer providers

Mistake 4: Not Checking Business Payment Rules

Some apps are designed for personal transfers, not business payments.

Freelancers should use methods suitable for professional income. This helps avoid:

- Account restrictions

- Payment holds

- Missing tax records

- Client payment disputes

- Poor documentation

Mistake 5: Keeping All Money in One Platform

Payment platforms are useful, but freelancers should regularly withdraw funds and keep savings in a trusted account.

A safer setup includes:

- One international receiving account

- One local business bank account

- One tax reserve account

- One emergency savings account

Mistake 6: Forgetting Tax Records

Choose payment methods that provide clear statements, transaction IDs, and downloadable records.

Good records help with:

- Tax filing

- Income proof

- Client disputes

- Business planning

- Loan or visa applications

- Accounting reports

Final Verdict

International money transfer fees can reduce your freelance income more than you realize. The cheapest option is not always the one with the lowest visible fee. You need to compare the full cost, including transfer fees, exchange-rate markups, withdrawal fees, and bank deductions.

Traditional banks are useful for large and formal transfers, but they can be expensive for small international freelancer payments. Wise can be strong for transparent currency conversion and multi-currency management. Payoneer is useful for marketplace payments and international receiving accounts. PayPal is convenient for clients but may cost more. Remittance apps are useful for personal transfers but not always ideal for business income.

For most international freelancers, the best approach is to use a multi-currency account for receiving global payments, a local business bank account for withdrawals and taxes, and a payment app or gateway only when the client needs extra convenience.

Before choosing a provider, always compare the final amount received. That is the number that matters most.

FAQs

What is the cheapest way to send money internationally?

The cheapest way depends on the sending country, receiving country, amount, currency, and payment method. Bank-funded online transfers are often cheaper than card-funded transfers or traditional wires, but you should compare the final received amount before sending.

Are banks more expensive for international transfers?

Banks can be more expensive for international transfers because they may charge wire fees, exchange-rate markups, and intermediary bank fees. However, banks may still be useful for large or formal business transfers.

Is Wise cheaper than a bank transfer?

Wise may be cheaper than many traditional bank transfers for certain currency routes because it often shows transparent fees and exchange rates. However, the actual cost depends on the currency, country, amount, and payment method.

Is Payoneer good for international freelancers?

Payoneer can be useful for international freelancers, especially those receiving payments from marketplaces, platforms, agencies, and global clients. Freelancers should compare receiving, conversion, and withdrawal fees before using it as their main payment method.

Is PayPal good for international payments?

PayPal is convenient and widely recognized, but it may have higher fees and currency conversion costs in some cases. It is often useful when clients prefer quick online payments, but it may not be the cheapest option.

What is an exchange-rate markup?

An exchange-rate markup is the difference between the real market exchange rate and the rate offered by a provider. It may not appear as a separate fee, but it reduces the amount received.

What are intermediary bank fees?

Intermediary bank fees are charges deducted by banks that help process an international wire transfer before it reaches the final recipient. These fees can be hard to predict.

How can freelancers avoid high transfer fees?

Freelancers can reduce fees by using local receiving details, comparing exchange rates, avoiding unnecessary conversions, choosing bank-funded transfers when cheaper, and withdrawing funds strategically.