Introduction

Cash flow is one of the biggest challenges for freelancers, consultants, digital agencies, and small businesses. You may have profitable projects, signed contracts, and unpaid invoices, but still struggle to pay expenses on time because client payments are delayed.

This is where financing options like a business line of credit and invoice factoring become important.

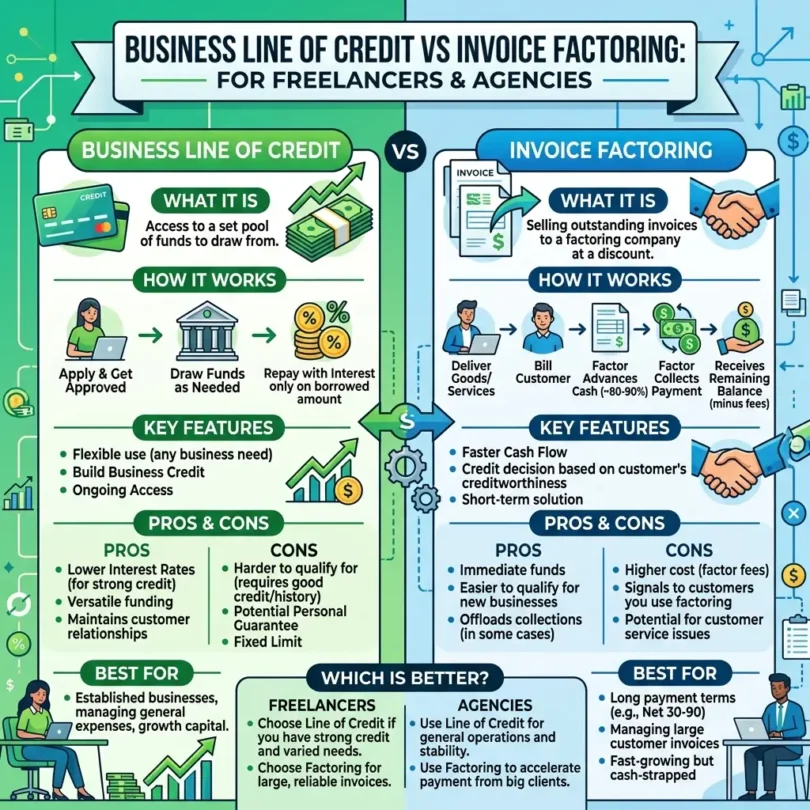

A business line of credit gives you access to flexible funds that you can draw from when needed. Invoice factoring allows you to sell unpaid invoices to a factoring company in exchange for faster cash. Both can help with working capital, but they work very differently.

For freelancers and agencies, the decision is not only about getting money quickly. You also need to think about:

- Fees

- Repayment terms

- Client relationships

- Credit requirements

- Business risk

- Contract terms

- Cash flow stability

- Long-term cost

- Tax and accounting records

A business line of credit may be better if you have stable revenue and want flexible access to funds. Invoice factoring may be better if you have unpaid invoices from reliable business clients and need cash before the payment due date.

However, both options come with risks. Borrowing money or selling invoices should never be treated casually. The goal is not to finance bad pricing, weak client contracts, or poor cash management. The goal is to solve short-term timing gaps while keeping your business financially healthy.

This guide compares business lines of credit and invoice factoring for freelancers, agencies, consultants, and small businesses. You will learn how each option works, when to use them, what fees to watch, and which option may be better for your situation.

What Is a Business Line of Credit?

A business line of credit is a flexible financing product that gives a business access to a set credit limit. You do not need to use the full amount immediately. Instead, you can draw funds when needed and usually pay interest only on the amount you use.

For example, if your business is approved for a $25,000 line of credit, you may draw $5,000 to cover payroll, software subscriptions, marketing costs, or contractor payments. You repay the borrowed amount, and depending on the structure, the available credit may become usable again.

BILL describes a business line of credit as flexible financing that gives a business access to a set amount of funds that can be pulled from as needed, with interest paid only on the amount used. (BILL)

A business line of credit can be used for:

- Short-term cash flow gaps

- Payroll

- Contractor payments

- Software subscriptions

- Marketing campaigns

- Emergency expenses

- Seasonal slow periods

- Inventory or equipment

- Client project costs

- Business expansion expenses

For freelancers and agencies, a line of credit can be helpful when payments are delayed but expenses are due now.

What Is Invoice Factoring?

Invoice factoring is a financing method where a business sells unpaid invoices to a factoring company. Instead of waiting 30, 45, 60, or 90 days for the client to pay, the business receives a percentage of the invoice value upfront.

The factoring company then collects payment from the client. After the client pays, the factoring company releases the remaining balance, minus fees.

A simple example:

- You invoice a client for $10,000.

- The invoice is due in 45 days.

- A factoring company advances 80% upfront.

- You receive $8,000 quickly.

- The client pays the factoring company later.

- The factoring company deducts fees.

- You receive the remaining balance after deductions.

Invoice factoring is different from a normal loan because the financing is based mainly on unpaid invoices and the creditworthiness of your clients. This can make it useful for agencies or B2B freelancers with strong clients but slow payment cycles.

Invoice factoring is often used by:

- Marketing agencies

- Staffing companies

- Logistics businesses

- Consultants

- B2B service providers

- Creative agencies

- IT service firms

- Contractors

- Businesses with long payment terms

However, invoice factoring may affect the client relationship because the factoring company may contact the client directly for payment.

Business Line of Credit vs Invoice Factoring: Main Difference

The main difference is simple:

A business line of credit is borrowed money that you repay.

Invoice factoring is selling unpaid invoices for faster cash.

A line of credit depends more on your business credit, revenue, financial history, and ability to repay. Invoice factoring depends more on your invoices and your client’s ability to pay.

Here is the basic comparison:

| Feature | Business Line of Credit | Invoice Factoring |

|---|---|---|

| Type | Revolving credit or flexible loan | Sale of unpaid invoices |

| Main purpose | Flexible working capital | Faster cash from unpaid invoices |

| Repayment | You repay borrowed funds | Client pays factoring company |

| Cost | Interest and fees | Factoring fee or discount rate |

| Based on | Credit, revenue, financials | Invoice quality and client credit |

| Client involvement | Usually private | Client may be notified |

| Best for | Flexible cash needs | Slow-paying B2B invoices |

| Risk | Debt and repayment pressure | Client relationship and factoring cost |

Why Freelancers and Agencies Consider These Options

Freelancers and agencies often deal with delayed payments. A client may approve work today but pay after 30 or 60 days. Meanwhile, the freelancer or agency still needs to pay for tools, contractors, ads, rent, internet, staff, and taxes.

Common cash flow problems include:

- Clients paying late

- Large invoices with long payment terms

- Monthly retainers paid after work is delivered

- Contractors needing payment before clients pay

- Software subscriptions due before revenue arrives

- Seasonal income drops

- Growing too quickly without enough cash

- Waiting for marketplace or platform payouts

- Unexpected tax bills

- Emergency business expenses

The Federal Reserve’s 2026 Report on Employer Firms found that 86% of small employer firms use financing on a regular basis, and the most common financing products include credit cards and loans. The same report noted that among firms with debt, 59% used a personal guarantee and 51% used business assets to secure debt. (FedSmallBusiness)

That matters because many small businesses do not use financing only for expansion. They use it to manage normal business operations, cover timing gaps, or stabilize cash flow.

How a Business Line of Credit Works

A business line of credit usually works in four steps.

1. Application

You apply with a bank, credit union, online lender, or fintech lender. The lender may review your:

- Business revenue

- Time in business

- Credit score

- Bank statements

- Tax returns

- Profit and loss statement

- Debt levels

- Business type

- Existing obligations

- Personal guarantee

Freelancers and small agencies may need to provide personal credit information, especially if the business is young or not formally incorporated.

2. Approval and Credit Limit

If approved, the lender gives you a credit limit.

Examples:

- $5,000

- $10,000

- $25,000

- $50,000

- $100,000+

The approved amount depends on your business strength, revenue, credit history, and lender criteria.

3. Draw Funds When Needed

You do not need to use the full amount. You can draw only what you need.

For example:

- Approved limit: $30,000

- Amount drawn: $6,000

- Remaining available credit: $24,000

You usually pay interest only on the amount you borrow, not the full approved limit.

4. Repay and Reuse

Many lines of credit are revolving. This means when you repay the borrowed amount, the available credit may become usable again.

This makes it useful for recurring short-term cash flow needs.

Business Line of Credit Fees and Costs

A business line of credit can include several costs.

Common fees include:

- Interest rate

- Draw fee

- Origination fee

- Maintenance fee

- Annual fee

- Late payment fee

- Prepayment fee in some cases

- Wire transfer fee

- Account servicing fee

- Personal guarantee risk

The cost depends on the lender, your credit profile, loan size, repayment term, and business strength.

A line of credit can be cheaper than some short-term financing options if you qualify for good rates. But if your credit is weak or the lender is high-cost, it can become expensive.

Pros of a Business Line of Credit

A business line of credit can be useful for freelancers and agencies that want flexible access to funds.

Key benefits:

- Flexible access to cash

- Use only what you need

- Interest usually applies only to borrowed amount

- Can help cover short-term expenses

- Useful for emergencies

- Can support business growth

- May improve cash flow planning

- Can be reused if revolving

- Client usually does not need to know

- Can help build business credit if reported properly

For agencies, a line of credit can help cover payroll or contractor costs before client payments arrive.

Cons of a Business Line of Credit

A line of credit is still debt. It must be managed carefully.

Main risks:

- Interest costs can add up

- Personal guarantee may be required

- Late payments can damage credit

- Variable rates may increase cost

- Easy access can encourage overspending

- Approval may be difficult for new freelancers

- Weak cash flow can make repayment stressful

- Some lenders charge multiple fees

- Secured lines may require collateral

The FTC advises small business borrowers to carefully evaluate financing offers, avoid rushing decisions, understand the total cost, and watch for misleading claims or terms that may not be clear upfront. (Federal Trade Commission)

This is especially important for freelancers because income can be irregular.

How Invoice Factoring Works

Invoice factoring usually works in five steps.

1. You Complete Work and Send an Invoice

First, you complete work for a business client and issue an invoice.

Example:

- Client: SaaS company

- Service: Monthly content marketing

- Invoice amount: $8,000

- Payment terms: Net 45

2. You Submit the Invoice to a Factoring Company

You send the unpaid invoice to a factoring company. The company reviews:

- Invoice amount

- Client creditworthiness

- Payment terms

- Your business history

- Dispute risk

- Client payment behavior

3. You Receive an Advance

If approved, the factoring company advances part of the invoice value.

Common advance rates may range from around 70% to 90%, depending on the company, industry, invoice quality, and client risk.

Example:

- Invoice value: $8,000

- Advance rate: 85%

- Upfront cash: $6,800

4. Client Pays the Factoring Company

The client pays the factoring company instead of paying you directly. In many factoring arrangements, the client is notified that payment should go to the factor.

This is one of the biggest differences between factoring and a line of credit.

5. You Receive the Remaining Balance Minus Fees

After the client pays, the factoring company deducts its fee and releases the remaining balance.

Example:

- Invoice value: $8,000

- Upfront advance: $6,800

- Factoring fee: $400

- Remaining release: $800

- Total received: $7,600

In this example, the cost of factoring is $400.

Invoice Factoring Fees and Costs

Invoice factoring costs are usually charged as a factoring fee or discount rate. The fee may depend on:

- Invoice amount

- Client payment speed

- Client credit quality

- Industry

- Factoring agreement

- Monthly invoice volume

- Recourse or non-recourse structure

- Contract length

- Whether the client pays late

Common cost factors include:

- Factoring fee

- Service fee

- Processing fee

- Wire fee

- Late payment fee

- Minimum volume fee

- Termination fee

- Due diligence fee

- Reserve holdback

The longer the client takes to pay, the more expensive factoring may become.

Pros of Invoice Factoring

Invoice factoring can be useful when your main problem is slow-paying clients.

Key benefits:

- Faster cash from unpaid invoices

- Approval may depend more on client credit than your credit

- Useful for B2B freelancers and agencies

- Can help cover payroll or contractor payments

- No traditional monthly loan payment in some structures

- Can support growth when invoices are strong

- Helpful for long payment terms

- May be easier than bank financing for newer businesses

For agencies working with corporate clients, factoring can help convert unpaid invoices into working capital faster.

Cons of Invoice Factoring

Invoice factoring can solve cash flow problems, but it also has downsides.

Main risks:

- Can be expensive

- Client may be contacted by factoring company

- May affect client relationship

- Fees can increase if clients pay late

- Contracts may require minimum invoice volume

- Some agreements are long-term

- Recourse factoring may require you to repay if client does not pay

- Not useful for B2C freelancers

- Not useful without unpaid invoices

- May signal cash flow weakness to clients

Factoring can also reduce control over client payment communication. For relationship-based freelancers and agencies, this matters.

Recourse vs Non-Recourse Factoring

Invoice factoring can be recourse or non-recourse.

Recourse Factoring

With recourse factoring, you may be responsible if the client does not pay.

For example:

- You factor a $10,000 invoice.

- The client refuses to pay.

- The factoring company may require you to buy back the invoice or repay the advance.

Best for:

- Businesses with reliable clients

- Lower-cost factoring arrangements

- Invoices with low dispute risk

Main risk:

You may still carry the risk if the client does not pay.

Non-Recourse Factoring

With non-recourse factoring, the factoring company takes on more risk if the client does not pay for certain approved reasons, such as insolvency. However, non-recourse does not always protect you from every situation.

For example, if the client refuses to pay because of a service dispute, you may still be responsible.

Best for:

- Businesses wanting more protection

- Invoices from strong clients

- Higher-risk payment environments

Main risk:

Non-recourse factoring may cost more and may include exclusions.

Always read the contract carefully.

Business Line of Credit vs Invoice Factoring: Which Is Cheaper?

There is no universal answer. The cheaper option depends on:

- Your credit profile

- Invoice amount

- Client payment speed

- Interest rate

- Factoring fee

- Repayment term

- How often you use financing

- Whether clients pay on time

- Additional fees

A business line of credit may be cheaper if:

- You qualify for a low rate

- You borrow only for a short time

- You repay quickly

- There are few extra fees

- You have stable revenue

Invoice factoring may be cheaper or easier if:

- You have strong unpaid invoices

- Your clients are reliable

- You do not qualify for a good line of credit

- You need money quickly

- You only factor invoices occasionally

But factoring can become expensive if clients pay slowly or if the contract includes extra fees.

Which Option Is Better for Freelancers?

For solo freelancers, a business line of credit is usually more flexible than invoice factoring. Many freelancers do not have large B2B invoices or corporate clients that factoring companies prefer.

A business line of credit may work better for freelancers who:

- Have stable income

- Need occasional cash flow support

- Want privacy from clients

- Have good credit

- Can repay quickly

- Need funds for software, tools, or emergencies

Invoice factoring may work for freelancers who:

- Work with business clients

- Send large invoices

- Have long payment terms

- Work with reliable companies

- Need cash before invoice due dates

- Do not qualify for traditional credit

For example, a freelance consultant with a $15,000 unpaid invoice from a corporate client may consider factoring. But a freelance logo designer with many small one-time clients may not be a good fit.

Which Option Is Better for Agencies?

Agencies often have more predictable B2B invoices, monthly retainers, contractors, payroll, and operating expenses. This can make both options useful, depending on the situation.

A business line of credit may be better for agencies that:

- Need flexible working capital

- Have recurring expenses

- Want to keep client payment relationships private

- Have strong revenue

- Can qualify for bank or fintech credit

- Need funds for payroll, ads, or contractor payments

Invoice factoring may be better for agencies that:

- Have large unpaid invoices

- Work with corporate clients

- Have net-30, net-45, or net-60 terms

- Need cash before clients pay

- Are growing quickly

- Have strong accounts receivable but limited cash

Example:

A marketing agency pays contractors weekly but receives client payments after 45 days. Invoice factoring may help bridge the gap if the client invoices are strong. A line of credit may be better if the agency wants flexible funds without involving clients.

When a Business Line of Credit Makes More Sense

A business line of credit may be the better choice when you need flexible access to cash, not just faster payment from invoices.

It may make sense if:

- You have stable monthly revenue.

- You want privacy from clients.

- You have good credit.

- You need funds for different business expenses.

- You want to cover temporary cash flow gaps.

- You can repay quickly.

- You want a reusable financing option.

- You do not want to sell invoices.

- You need money before you even issue invoices.

A line of credit is often better for general working capital.

When Invoice Factoring Makes More Sense

Invoice factoring may be better when your main problem is unpaid invoices.

It may make sense if:

- You already completed the work.

- You already issued invoices.

- Your clients are businesses, not consumers.

- Your clients are creditworthy.

- You have long payment terms.

- You need cash quickly.

- You do not qualify for a line of credit.

- You are comfortable with client notification.

- Your invoice amounts are large enough to justify the cost.

Factoring is often better for accounts receivable cash flow.

Safer Alternatives to Consider First

Before using a line of credit or invoice factoring, freelancers and agencies should consider lower-risk cash flow strategies.

1. Require Deposits

Ask for a deposit before starting work.

Common deposit structures:

- 25% upfront

- 30% upfront

- 50% upfront

- 100% upfront for small projects

Deposits reduce the amount of unpaid work you finance yourself.

2. Use Milestone Payments

For larger projects, divide payment into stages.

Example:

- 30% before starting

- 40% after first milestone

- 30% before final delivery

This reduces risk and improves cash flow.

3. Shorten Payment Terms

Instead of net-60 or net-45, consider:

- Due on receipt

- Net-7

- Net-15

- Net-30

Shorter terms help reduce financing needs.

4. Offer Early Payment Discounts

You can offer a small discount for faster payment.

Example:

- 2% discount if paid within 7 days

- Full amount due within 30 days

This can be cheaper than factoring in some cases.

5. Add Late Payment Terms

Clear late payment terms encourage clients to pay on time.

Your contract and invoice may include:

- Payment due date

- Late fee policy

- Work pause policy

- Transfer fee responsibility

- Final delivery terms

- Collection process

Check local laws before applying late fees.

6. Build a Cash Reserve

A cash reserve is the safest form of working capital.

Aim to build:

- 1 month of expenses

- 3 months of expenses

- 6 months of expenses over time

This reduces dependence on financing.

7. Improve Client Screening

Some cash flow problems come from poor clients, not poor financing.

Before accepting a project, check:

- Does the client have a real business?

- Do they agree to written terms?

- Do they pay deposits?

- Do they have a history of slow payment?

- Are they clear about scope?

- Do they avoid payment discussions?

Better clients reduce financing pressure.

Red Flags to Watch Before Choosing Financing

Before choosing a business line of credit or invoice factoring, watch for warning signs.

Red flags include:

- No clear APR or total cost

- Pressure to sign quickly

- Confusing repayment terms

- Hidden fees

- Very high daily or weekly repayment pressure

- Required personal guarantee without clear explanation

- Long contract lock-in

- Minimum volume requirements

- Large termination fees

- Unclear client notification process

- No written fee schedule

- Vague promises of “guaranteed approval”

The FTC has warned small business borrowers to avoid rushing into financing decisions and to carefully review offers, repayment terms, and total cost. (Federal Trade Commission)

Business Line of Credit vs Invoice Factoring: Practical Examples

Example 1: Freelance Developer

A freelance developer earns $8,000 per month from multiple clients. One client pays late, and the freelancer needs $2,000 for software, rent, and contractor support.

A small business line of credit may be better because the freelancer needs flexible cash and does not have one large invoice suitable for factoring.

Example 2: Marketing Agency

A marketing agency has a $40,000 invoice due from a corporate client in 60 days. The agency needs money now to pay contractors and ad operations staff.

Invoice factoring may be useful if the client is reliable and the factoring cost is lower than the cost of delaying operations.

Example 3: SEO Consultant

An SEO consultant has stable monthly retainers but wants extra cash for a new website, tools, and a short-term hiring need.

A business line of credit may be better because the funds are needed for general growth, not one unpaid invoice.

Example 4: Creative Agency With Slow Corporate Clients

A creative agency works with large companies that always pay, but only after 60 or 90 days. The agency has strong invoices but weak cash flow.

Invoice factoring may help if the agency accepts the fee and client notification process.

Comparison Table: Which One Should You Choose?

| Situation | Better Option |

|---|---|

| You need flexible funds for many expenses | Business line of credit |

| You have large unpaid B2B invoices | Invoice factoring |

| You want clients to stay uninvolved | Business line of credit |

| You have weak credit but strong clients | Invoice factoring |

| You need money before sending invoices | Business line of credit |

| You need cash from completed work | Invoice factoring |

| You want reusable credit | Business line of credit |

| You want financing based on receivables | Invoice factoring |

| You work mostly with consumers | Business line of credit |

| You work with corporate clients on net terms | Invoice factoring |

Final Verdict

A business line of credit and invoice factoring can both help freelancers, agencies, and small businesses manage cash flow, but they solve different problems.

A business line of credit is usually better when you want flexible working capital, privacy from clients, and the ability to borrow only what you need. It can be useful for freelancers, consultants, and agencies with stable revenue and the ability to repay borrowed funds.

Invoice factoring is usually better when your cash flow problem comes from unpaid B2B invoices. It can help agencies and service businesses unlock cash from invoices before clients pay, but it may cost more and may involve direct contact with your clients.

For most freelancers, the safest first step is not financing. It is better payment structure:

- Request deposits.

- Use milestone payments.

- Shorten payment terms.

- Offer easy payment options.

- Build a cash reserve.

- Track invoices carefully.

- Avoid slow-paying clients.

If you still need financing, compare the total cost, not just the advertised rate. Read the contract carefully, understand the repayment terms, and choose the option that solves your actual cash flow problem without creating a bigger one.

FAQs

What is better: a business line of credit or invoice factoring?

A business line of credit is usually better for flexible working capital. Invoice factoring is better when your main problem is unpaid B2B invoices from reliable clients.

Is invoice factoring a loan?

Invoice factoring is not usually structured as a traditional loan. It is commonly treated as selling unpaid invoices to a factoring company in exchange for faster cash.

Is a business line of credit good for freelancers?

A business line of credit can be useful for freelancers with stable income and good repayment ability. It can help cover short-term cash flow gaps, but it should be used carefully because it is still debt.

Is invoice factoring good for freelancers?

Invoice factoring may work for freelancers with large unpaid invoices from business clients. It is less useful for freelancers with many small consumer clients or one-time projects.

Does invoice factoring hurt client relationships?

It can affect client relationships because the factoring company may contact the client or require the client to pay them directly. This depends on the factoring arrangement.

Is invoice factoring expensive?

Invoice factoring can be expensive, especially if clients pay slowly or the agreement includes extra fees. Always compare the total cost before signing.

Do business lines of credit require personal guarantees?

Many small business lines of credit may require a personal guarantee, especially for newer businesses or businesses without strong credit history. The Federal Reserve’s 2026 small business report noted that personal guarantees are common among firms with debt. (FedSmallBusiness)

Can an agency use invoice factoring?

Yes, agencies can use invoice factoring if they have unpaid invoices from reliable business clients. It may help cover contractor payments, payroll, and operating expenses while waiting for clients to pay.

What is the safest alternative to invoice factoring?

The safest alternatives include deposits, milestone payments, shorter payment terms, early payment discounts, strong contracts, and building a cash reserve.

What should I check before applying for business financing?

Check the total cost, repayment terms, fees, personal guarantee, contract length, late payment rules, client notification requirements, and whether the financing solves your real cash flow problem.